Trevor stared at his coffee receipt and felt his stomach drop. $6.85 for a medium latte and pastry. Again. It was the third time this week, and suddenly he was doing math in his head that he didn’t want to face.

“I kept telling myself it was just coffee,” Trevor said later, scrolling through his banking app. “Seven bucks here, seven bucks there. It felt like pocket change until I actually added it up.”

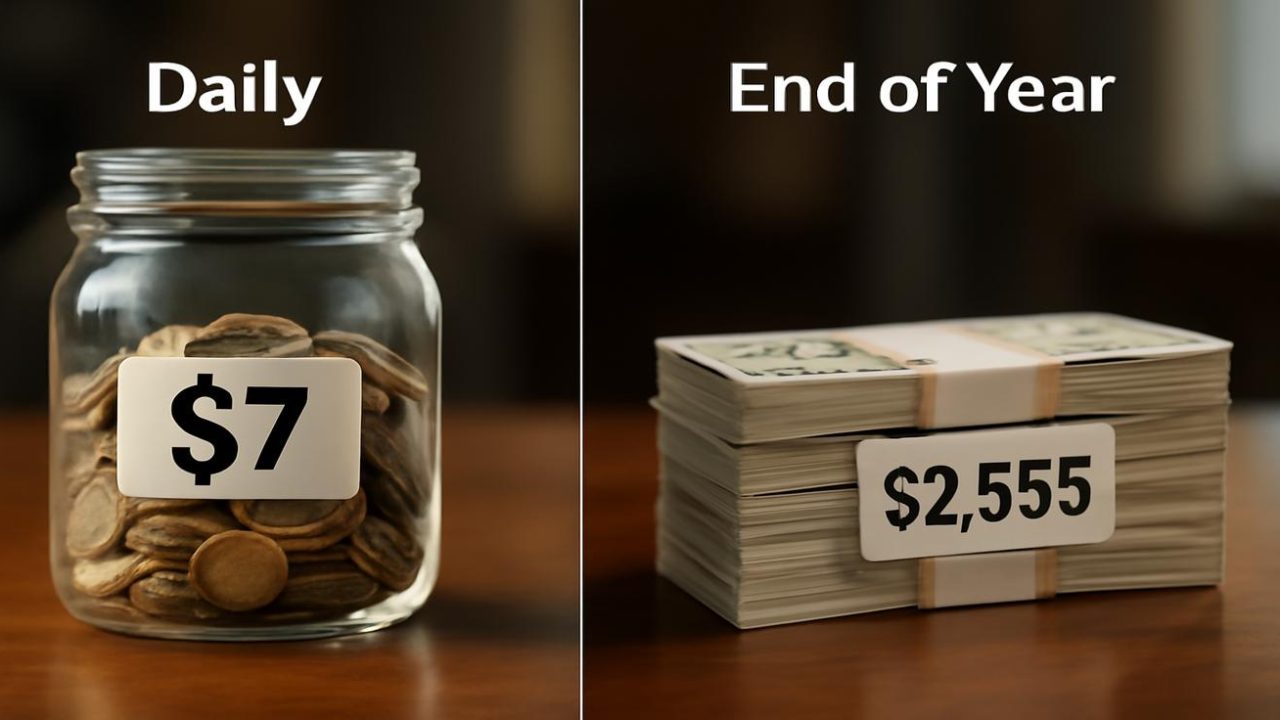

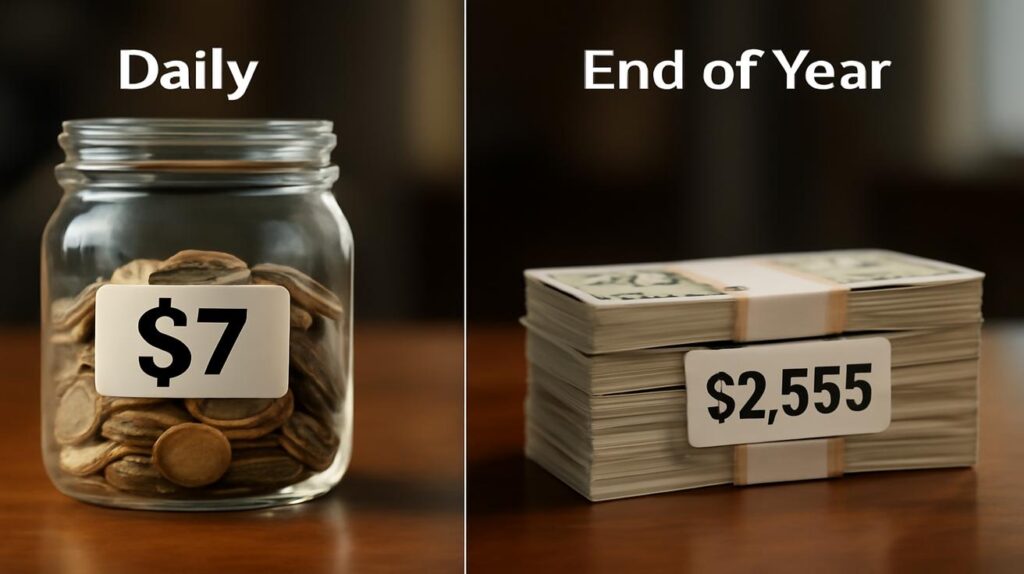

The numbers were brutal. Those seemingly innocent daily purchases had quietly drained $2,555 from his account over the year. Trevor isn’t alone in this wake-up call that’s hitting millions of Americans who are finally connecting the dots between small daily expenses and major financial impact.

The $7 Daily Habit That’s Costing You Thousands

When you break down $7 a day, it sounds manageable. Most people spend more than that on lunch without thinking twice. But here’s where the math gets uncomfortable: $7 daily equals $49 weekly, $196 monthly, and a staggering $2,555 annually.

Financial experts call this “lifestyle creep” – the gradual increase in spending that happens so slowly we don’t notice until it’s too late. Whether it’s premium coffee, lunch delivery, streaming services, or convenience store runs, these micro-expenses add up faster than most people realize.

Most people can visualize spending $2,500 on something big, but they can’t see how $7 disappears every single day. It’s psychological – small amounts don’t trigger our financial alarm bells.

— Jennifer Martinez, Certified Financial Planner

The pandemic made this problem worse. With more people working from home, delivery apps and subscription services became daily habits. What started as occasional treats became routine expenses that many forgot to track.

Where Your Daily Seven Dollars Really Goes

Understanding exactly how $7 daily habits drain your finances requires looking at the most common culprits. Here’s how different $7 expenses compound over time:

| Daily Expense | Weekly Cost | Monthly Cost | Annual Cost |

|---|---|---|---|

| Coffee shop visits | $49 | $210 | $2,555 |

| Lunch delivery fees | $49 | $210 | $2,555 |

| Convenience store snacks | $49 | $210 | $2,555 |

| Parking fees | $49 | $210 | $2,555 |

| Vending machine purchases | $49 | $210 | $2,555 |

The most dangerous daily expenses share common characteristics:

- They feel necessary or justified in the moment

- They’re purchased with cards, making spending less tangible

- They happen at the same time or place, becoming automatic

- They’re small enough to avoid budget scrutiny

- They provide immediate satisfaction or convenience

I tell my clients to track every purchase under $10 for one week. They’re always shocked by what they find. It’s not about depriving yourself – it’s about awareness.

— Robert Chen, Personal Finance Coach

Many people discover they have multiple $7 daily habits running simultaneously. Someone might spend $7 on coffee, another $7 on lunch delivery fees, and $7 on evening snacks. That’s $21 daily, or $7,665 annually – enough for a significant emergency fund or vacation.

The Real Impact on Your Financial Future

Beyond the immediate drain on your checking account, daily $7 habits represent massive opportunity cost. That $2,555 annually could transform your financial picture in multiple ways.

If invested in a basic index fund averaging 7% annual returns, that $2,555 would grow to approximately $5,100 in 10 years. Over 20 years, it becomes $9,870. For a 25-year-old, eliminating one $7 daily habit and investing the money instead could mean an extra $51,000 at retirement.

People think about coffee money as gone forever, but that’s not true. Every dollar you don’t spend on unnecessary daily purchases is a dollar that can compound and grow for decades.

— Lisa Thompson, Investment Advisor

The psychological impact matters too. Many people report feeling more in control of their finances once they identify and address their daily spending leaks. It’s not about eliminating all small pleasures, but about making conscious choices rather than falling into expensive autopilot habits.

Some find that tracking daily expenses reveals patterns they never noticed. Maybe they only buy expensive coffee when stressed, or order delivery when they’re too tired to cook. Understanding these triggers helps create better financial habits.

Breaking the $7 Daily Cycle

The good news is that small daily expenses are often the easiest to modify because they don’t require major lifestyle changes. Simple swaps can save thousands while maintaining similar satisfaction:

- Brew coffee at home and invest in a quality travel mug

- Pack snacks instead of buying them at convenience stores

- Use free parking apps to avoid daily parking fees

- Meal prep to reduce lunch delivery temptation

- Cancel automatic subscriptions you rarely use

The key is replacing the habit, not just eliminating it. If your $7 coffee run provides a morning routine you enjoy, create a new routine around making coffee at home. If delivery apps solve your dinner decision fatigue, batch cook meals on weekends instead.

Success comes from substitution, not deprivation. Find cheaper ways to get the same emotional or practical benefit, and the savings happen naturally.

— Michael Rodriguez, Behavioral Finance Expert

Some people benefit from automating their savings by setting up a daily $7 transfer to a separate account. This “pay yourself first” approach ensures the money goes toward financial goals before it can be spent on impulse purchases.

FAQs

How can I track my daily $7 expenses without obsessing over every purchase?

Use a simple app or write down purchases under $10 for just one week to identify patterns, then focus on your biggest spending triggers.

Is it realistic to eliminate all small daily purchases?

No, and you shouldn’t try. The goal is awareness and intentional spending, not deprivation of all small pleasures.

What if my $7 daily habit is something I really enjoy?

Consider reducing frequency rather than eliminating it entirely – maybe premium coffee three times per week instead of daily.

How long does it take to break a daily spending habit?

Most people see results within 2-3 weeks of consistent effort, but it takes about 60 days to fully establish new financial habits.

Should I invest the money I save or pay off debt first?

Generally, pay off high-interest debt first, then build an emergency fund, then invest – but consult a financial advisor for personalized advice.

What’s the easiest $7 daily habit to eliminate?

Subscription services you rarely use or convenience store purchases that could easily be bought cheaper in bulk at grocery stores.

Leave a Comment